A Data-Driven Guide for Navigating the 2026 Oil Price Shock

By Peter Niculescu and Leslie Rahl

Published in Law360 on April 17, 2026.

In the span of just three weeks, the price of West Texas Intermediate crude oil surged from approximately $70 per barrel to nearly $100, as U.S. and Israeli joint strikes on Iran starting on Feb. 28 disrupted tanker traffic through the Strait of Hormuz.

Since then, prices have continued to climb, reaching $111.54 per barrel on April 2.

Oil market volatility as measured by the Cboe Crude Oil Volatility Index, or OVX, has surged to near its second-highest level since 2010, exceeded only by the COVID-driven demand collapse of March and April 2020.

For attorneys advising clients in energy, commodities, finance and commercial litigation, this episode of extreme price dislocation is likely to generate a significant wave of complex legal disputes.

We have previously served as experts in multiple billion-dollar equity volatility matters, and have advised clients in sugar, copper, energy and fixed income disputes. Today's environment is different in character, but equally consequential. The history of market volatility tells us disputes and litigation are likely.

Understanding the Shock: What the Data Actually Shows

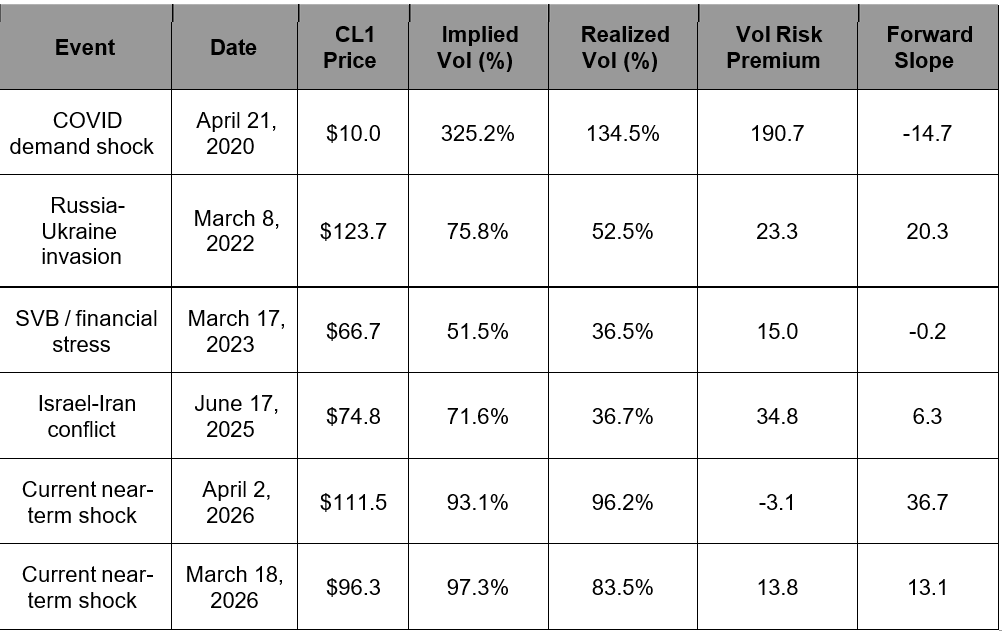

While the price spike is well-known, its scale in historical context may not be as well appreciated. The current oil shock is supply-driven, with geopolitical risk playing the primary role, and demand dynamics, which are under pressure from global trade headwinds and softening U.S. labor markets, providing a secondary, complicating force.

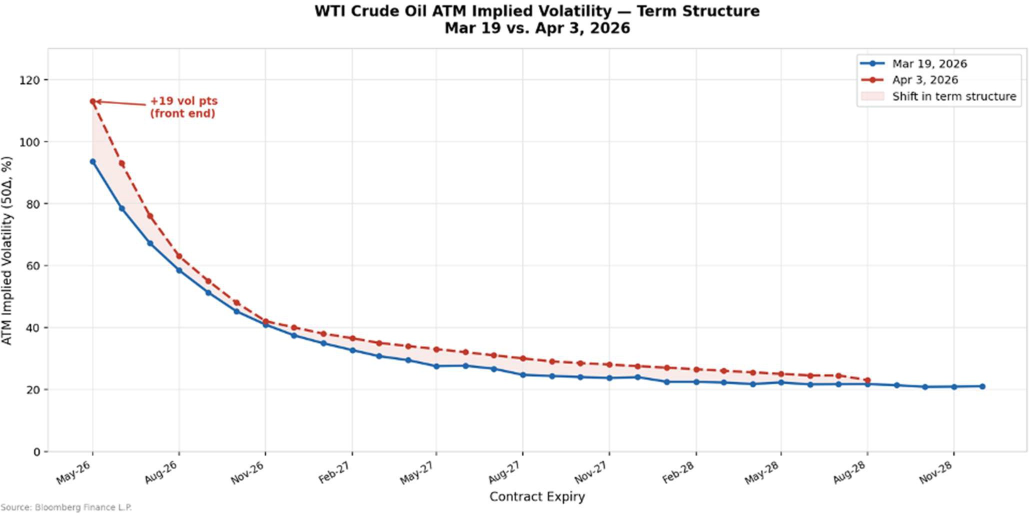

Front-end implied volatility is elevated compared to most recent shocks. The table below benchmarks the current market against four comparable historical episodes, using WTI front-month (CL1) pricing, the OVX implied volatility index, 20-day realized volatility, the volatility risk premium (implied minus realized) and the forward curve slope (CL1 minus CL6).

Two features of the current volatility surface are particularly significant for litigation purposes.

First, the steep term structure, with near-term implied volatility well above longer-dated levels, means the market is pricing a concentrated front-end supply shock, and expects uncertainty to resolve over the next three to six months.

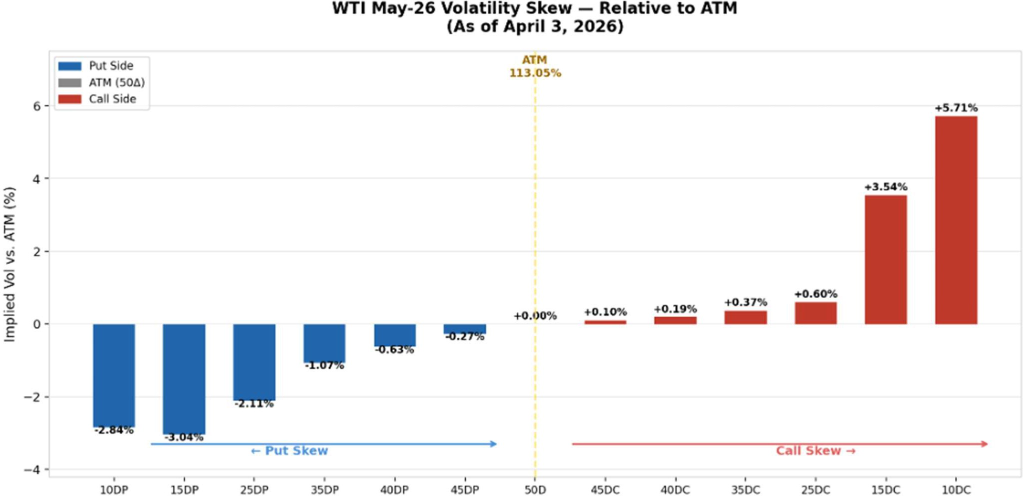

Second, there is now only a small call skew. A call skew happens when options that go into the money at higher than current prices — i.e., that have higher "strikes" — have higher implied volatilities than options with strikes at current prices.

The implied volatilities of options with very high strikes are now slightly higher than the implied volatility of options struck at the money. The market currently assesses the risks of a further breakout to the upside to be slightly higher than the risks of a resolution to the crisis, whereas two weeks ago, the market assessed a much higher risk of a further spike in oil prices.

This is the opposite profile from the COVID crisis, which produced steep volatility skew as demand destruction risk dominated.

The volatility risk premium, which is the gap between what the market is paying for protection and what volatility has realized recently, has now turned negative.

Unlike prior stress episodes such as Russia-Ukraine or Israel-Iran, where implied volatility significantly exceeded realized volatility, the present environment does not reflect a pronounced premium for optionality.

This suggests that current option pricing is in line with observed market conditions, rather than reflecting elevated risk premia. This distinction may be relevant in assessing whether counterparties' valuation and risk management decisions during the period were consistent with prevailing market conditions.

Five Legal Battlegrounds Counsel Should Prepare for Now

History tells us that extreme commodity volatility generates disputes in predictable categories. Each of the following areas is already generating inquiries to our team, and litigation pipelines will build over the coming months.

Hedging Failures and Margin Call Disputes

The most immediate source of disputes will be hedging failures, particularly from investors in companies and funds caught underhedged by the sudden price surge, and margin call conflicts arising from volatility-driven collateral demands.

In options markets, implied volatility compounds the impact of a price spike. A position that looked adequately margined at 40% OVX is dramatically undermargined at 100% OVX.

Once counterparties have been placed on notice of current market conditions, further risk management errors become harder to forgive legally.

Disputes will turn on whether margin calls and automatic termination events under International Swaps and Derivatives Association agreements were properly triggered, and whether closeout valuations were conducted at commercially reasonable prices during an illiquid crisis-period market.

Derivatives Valuation and Price Benchmark Conflicts

Illiquid markets make pricing complex financial instruments contentious. For structured products tied to or affected by oil price indices, the question of which valuation methodology applies when underlying markets are dislocated from normal functioning will be vigorously contested.

Separately, price benchmark conflicts, which involve challenges to price formulas and benchmark calculations used in long-term supply contracts or derivative settlements, become acute when realized prices diverge dramatically from historical norms.

Force Majeure and Material Adverse Change Claims

The closure of the Strait of Hormuz is precisely the kind of extraordinary event that prompts counterparties to invoke force majeure clauses across oil supply contracts, liquefied natural gas purchase agreements, commodity derivative transactions and financing arrangements.

Litigation over these invocations will turn on whether performance was genuinely impossible or merely more expensive, whether the disruption was truly unforeseeable given escalating Middle East tensions, and whether reasonable mitigation steps were taken.

Material adverse change clauses in M&A and credit agreements tied to energy sector companies will face similar scrutiny.

Damages Quantification: The Counterfactual Problem

In any commodity-related damages case, the core question is: What would have happened but for the alleged wrong? In the current environment, that question is exceptionally hard to answer.

The trajectory of oil prices in 2026 is so path-dependent on geopolitical events that standard damages methodologies risk producing arbitrary results. Expert damages analysis must center on three issues:

· Valuation of illiquid derivatives in turbulent markets;

· Estimating lost profits from price spikes without overly smoothed benchmarks that mask realized volatility; and

· Calculating hedge failures and collateral costs, including the interaction between oil prices, refinery margins and downstream product pricing.

Market Manipulation and Regulatory Investigations

Crisis-period markets historically attract regulatory scrutiny from the Commodity Futures Trading Commission, the U.S. Securities and Exchange Commission and international regulators.

Enforcement actions will examine whether traders exploited the price spike through manipulation of futures markets, improper front-running or abuse of dominant positions in physical markets.

Public companies with significant oil price exposure that had inadequate hedges, or failed to update risk factor disclosures as tensions escalated, may also face securities litigation.

Three Forward Scenarios, and Why Each Creates Its Own Dispute

The current volatility surface gives us important forward guidance: Markets are pricing a concentrated near-term supply shock and expect the uncertainty to resolve within months.

But the range of outcomes is wide. Each of the three plausible scenarios carries a distinct litigation profile.

Scenario 1: Persistent Supply Shock

Should the disruption last longer than the volatility surface currently implies, parties may be caught underhedged. If the shock evolves into a longer-lasting issue, a larger repricing could occur in longer-dated oil prices and midcurve volatilities, not just the front end.

The Organization of the Petroleum Exporting Countries supply-cut episode of April 2023 provides a precedent: Mid-term volatility remained elevated rather than collapsing, wrong-footing positions structured for a quick recovery.

Disputes in this scenario will center on failure to supervise and escalate risk management decisions as the crisis deepened.

Scenario 2: Rapid Geopolitical Resolution

The opposite risk is that the crisis resolves suddenly. If the Strait of Hormuz reopens, or if supply disruptions ease more quickly than expected, markets may have priced a stronger near-term supply shock. Oil prices could drop sharply while implied volatility compresses simultaneously.

The June 2025 Israel-Iran episode is the relevant precedent, where both spot and implied volatility reversed sharply lower after ceasefire headlines, causing long call and long front-end volatility positions to suffer significant losses.

Parties holding overpriced protection will seek to unwind or dispute valuations. Those who wrote that protection may claim their counterparties failed to act in good faith during the spike.

Scenario 3: Demand Slowdown Shifts the Narrative

The market is currently focused on supply risk, but a macro narrative shift is possible. U.S. labor data already show softening: February nonfarm payrolls fell by 92,000, and unemployment rose to 4.4%.

And if recession concerns build, the narrative could pivot from supply disruption to demand destruction.

In that environment, oil prices could stabilize or fall sharply, hurting long option positions and generating a fresh round of disputes from parties that structured hedges for a sustained high-price environment.

Practical Guidance: Data Is King

Besides effective risk management and sound legal analysis, what can companies do right now to protect themselves in a future dispute? The answer is straightforward: Preserve every scrap of market data available to you. In disputes of this kind, data is king.

Pricing data, particularly intraday data from the period of extreme volatility, is notoriously difficult to reconstruct after the fact.

Courts and arbitrators need to understand what the market looked like at the precise moment a margin call was triggered, a closeout valuation was taken or a force majeure notice was issued. The further in time from the event, the harder that reconstruction becomes.

Advise clients now to preserve intraday price and volatility data, order book depth and bid/offer spreads, open interest data across maturities, broker and dealer communications, axe sheets, contributor information to index pricing, and all internal risk management escalation records from the February-March period.

In disputes involving options and structured products, the volatility surface itself — not just spot prices — is critical evidence. The current surface, with its steep near-term decay and pronounced call skew, tells a specific story about market expectations at any given moment.

Parties that fail to preserve this data will find themselves at a significant disadvantage when experts reconstruct "what the market was saying" at the time of the disputed transaction or closeout.

The historical pattern across the Russia-Ukraine war, Israel-Iran tensions and the COVID crisis all confirm the same lesson: Clients and counsel best positioned in subsequent litigation are those who treated data preservation as a live exercise, not a retrospective one.

Peter Niculescu is a partner and the lead testifying expert at Capital Market Risk Advisors Inc.

Leslie Rahl is the founder and CEO of the firm.

The opinions expressed are those of the author(s) and do not necessarily reflect the views of their employer, its clients, or Portfolio Media Inc., or any of its or their respective affiliates. This article is for general information purposes and is not intended to be and should not be taken as legal advice.